‘Triple Shock’ Intensifies Deflationary Pressures in China, Government Stimulus Faces Limits

Input

Modified

August Slump in Production, Consumption, and Investment Decline in Fixed-Asset Investment Including Infrastructure Annual GDP Growth Target of 5% Under Strain

China’s production, consumption, and investment all fell short of market expectations in August, registering a “triple shock.” As the export boom that supported the economy in the first half of the year fades, the likelihood of a slowdown in the second half has materialized, putting the government’s target of roughly 5% growth at risk.

Prolonged Weakness in Production, Consumption, and Investment

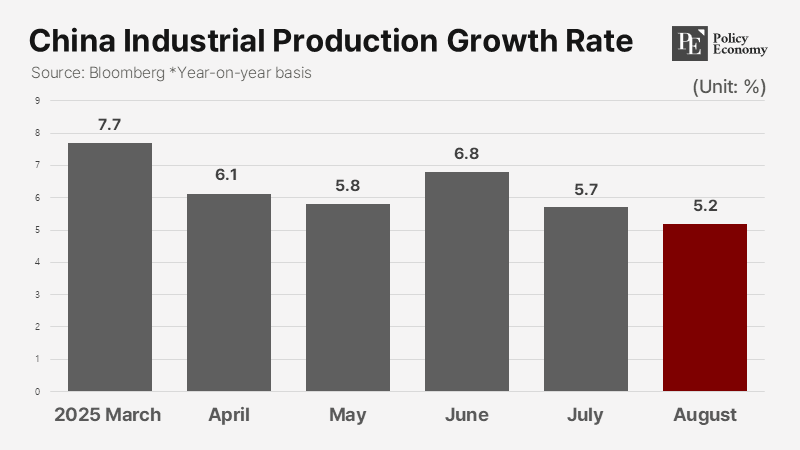

According to the National Bureau of Statistics on the 16th, August industrial production rose only 5.2% year-on-year, missing the market forecast of 5.7%. It was the weakest pace since August last year (4.5%). Growth in industrial output has been decelerating steadily since March (7.7%). Retail sales, a barometer of domestic demand, increased just 3.4% year-on-year in August, below both market expectations (3.8%) and July’s pace (3.7%), marking the lowest since November last year (3%).

Fixed-asset investment for January–August rose just 0.5% from a year earlier, far below the forecast of 1.5% and the 1.6% growth seen in January–July. Fixed-asset investment—spanning factories, roads, and power grids—has contracted rapidly: 4.2% in March, 3.7% in May, 2.8% in June, 1.6% in July, and finally down to 0% in August. Analysts attribute this to government restrictions aimed at addressing supply glut issues, which in turn curbed investment momentum.

Prices are also in decline. Consumer prices, which had been negative from February through May, ticked up by 0.1% in June, but fell back to 0% in July and slipped to -0.4% in August, renewing deflationary pressure. Real estate investment remains deeply depressed. Property development spending for January–August dropped 12.9% year-on-year—the worst performance since the 2021 Evergrande crisis, when developers burdened with over $280 billion in debt triggered a sector-wide meltdown. Nationwide urban unemployment rose to 5.3% in August, above both forecasts (5.2%) and the July reading (5.2%).

The statistics bureau acknowledged that China’s economy faces “numerous risks and challenges” from a volatile external environment, yet markets interpret the situation as even more severe. Economic indicators were already at their worst of the year in July, and deteriorated further in August. Exports in August increased only 4.4% year-on-year, lagging both market expectations (5.0%) and July’s growth (7.2%).

Deepening Deflationary Pressures

With production, consumption, and investment all faltering, markets are bracing for a sharper slowdown in the second half. The suspension of mutual tariffs by the United States had pulled forward some export demand, helping China’s GDP expand 5.3% year-on-year in the first half. But with that effect fading and tariff battles set to intensify, Beijing’s 5% growth target looks increasingly untenable. Moreover, the base effect of last September’s large-scale stimulus will likely amplify deflationary pressure in the second half.

China now faces downward pressure on prices from both weak demand and persistent industrial overcapacity. Household purchasing power is eroding, while excessive production capacity across industries continues, compounding deflationary risk. Overcapacity has not only distorted China’s domestic economy but has also become a global issue, as cheap Chinese goods flood foreign markets and erode industrial competitiveness abroad.

The United States has already pressed Beijing to address overcapacity in trade negotiations earlier this year, while European countries have also demanded reductions. Yet trade uncertainty has discouraged firms from offloading inventory, leading companies to hold rather than cut stockpiles, thereby perpetuating the supply glut.

Need to Curb Overcapacity and Cut-Throat Competition

In response, Beijing has launched campaigns to curb “involution”—destructive internal competition driven by excessive price wars. This year, the government rolled out the Fair Competition Review regulation, revised rules on payments between large and small enterprises, amendments to the Anti-Unfair Competition Law, and revisions to the Pricing Law. The narrowing decline in the producer price index—from -3.6% in July to -2.9% in August—can be interpreted as a modest outcome of these efforts. Still, with PPI in negative territory for 35 consecutive months, the underlying problem remains unresolved. Manufacturing overcapacity, in particular, continues to weigh on prices.

Persistent price declines risk prompting consumers to delay purchases while undermining corporate investment appetite, dragging on growth. This has fueled calls for more aggressive government stimulus. Yet economists caution that China’s challenges cannot be solved by short-term stimulus alone. Rather, a structural reset of overcapacity, combined with policies that foster private-sector innovation and investment, is necessary. However, reducing production capacity entails job losses, which in turn weaken consumption—a dilemma that underscores the difficult bind facing China’s policymakers.

Similar Post

Comment